Following the SEC’s 568 pages of proposed rules for Title III Crowdfunding, I released a comparison chart highlighting the benefits and drawbacks of selected crowdfinance offerings including 506c offerings, proposed Title III Crowdfunding, Intrastate Crowdfunding and Registered Crowdfunding.

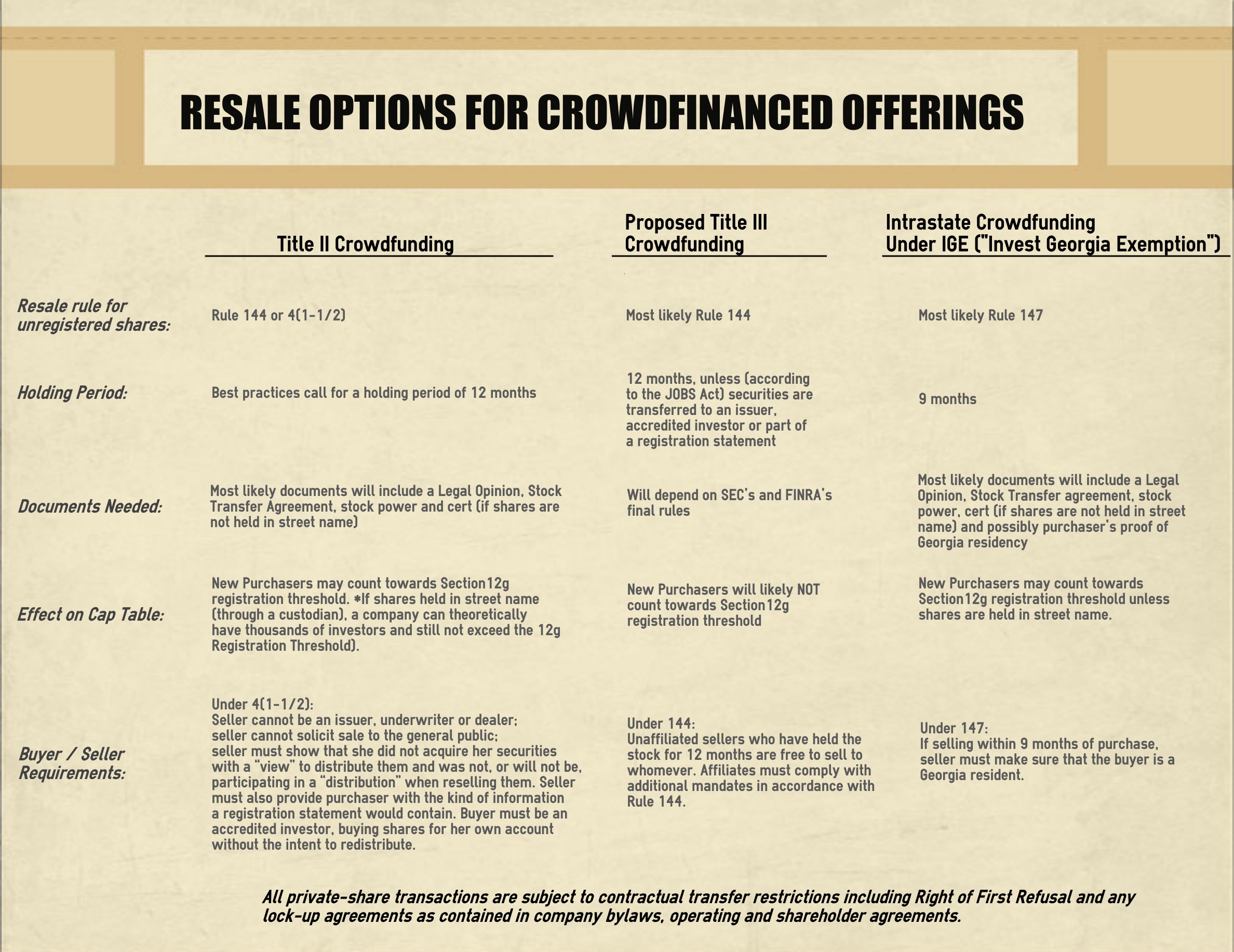

In addition to rousing a great deal of interest in Wall Street’s latest corporate finance structures, the chart led to a number of discussions and inquiries relating to liquidity and secondary transactions. As a result, I am pleased to provide the industry with a subsequent chart analyzing the resale options for private stock obtained through crowdfinance offerings, along with a roadmap to a practicable secondary marketplace for privately-held shares.

Although pertinent to the construction of a secondary exchange, the ability to resell private stock is only part of the equation. The quintessential components will lie in the procurement of the underlying infrastructure. In order for a secondary marketplace for private shares to effectively flourish, it must possess dependable settling and clearing functionality, reliable certificate tracking, issuer transparency, and an ecosystem of support from brokers, market makers, impartial research analysts and most importantly, from the mounting “crowd” of retail investors.

Without this stable foundation, the marketplace for private shares will remain as disorganized and fragmented as it was during the frenzied weeks leading up to Facebook’s IPO (read: https://daraalbright.com/2012/01/09/chasing-spreads-in-private-company-secondary-transactions/).

INFRASTRUCTURE – The panacea for private share secondary transactions

The infrastructure to support private-share secondary transactions is rapidly developing. In addition to operating a secondary platform for p2p loans, Folio Institutional currently provides clearing, custody and settlement solutions for private placements. Brokerage firms, facilitating 506c offerings through Folio, provide issuers with an added benefit: the ability to remain under the 12g registration threshold regardless of the number of investors that end up participating in the offering. By holding all investors’ shares in the name of the broker / dealer as opposed to the individual investor, issuers can theoretically maintain a liquid secondary market for its stock while remaining private indefinitely.

As private companies become more accessible to the public, demand for transparency is on the rise. With the SEC’s implementation of title II of the JOBS Act, for the first time in eight decades, private issuers are not only permitted, but encouraged, to publicly share information about its business. Thousands of private companies are now utilizing the new 506c exemption in order to market their offerings to the public.

Finally, I think it is important to address the ongoing recommendations for the creation of a new private share exchange exclusively for accredited investors. I think this would be a mistake of gargantuan proportions as the last thing our financial markets need is more inequality. In order to maintain a democratic, vibrant and reputable secondary marketplace for private shares, our legislators should consider significant changes to the discriminatory accredited investor rule. Instead of basing accreditation on income levels and net worth, they should base it on knowledge and experience. As the nation’s wealth gap widens more with each passing day, America can no longer continue denying its smaller investors the same investing privileges it allows its wealthier ones. With public stock markets stacked to benefit large corporate entities and institutional buyers, the government cannot keep relying on private-equity prohibition to protect investors. Instead of punishing the very investors who can provide the small business capital necessary to foster economic growth, regulators should simply consider harsher penalties for fraudulent behavior.

I’d like to thank Mitchell Littman, Founding Partner at Littman Krooks, a New York based law firm with distinct expertise in private secondary transactions, as well as Jeff Bekiares, co-founder of SparkMarket and legal specialist in intrastate crowdfunding for their assistance in the creation of the chart analyzing the various resale options for crowdfinanced offerings.

Leave a Reply