One day — in the not too distant future — crypto will completely displace equities as an asset class. Yes, you read that correctly. Our beloved equities will soon join the club of obsoletion where the phone booth, the Walkman, the floppy disk, the Fotomat, the VCR, the fax machine, and many others reminisce about their youth while watching their … Read More

Skip links

Dara Albright Media

Dara Albright Media is known for its trendsetting FinTech articles and acclaimed industry conferences that helped birth the crowdfinance movement.

As Seen In…

Dara Albright Media

Enlightment

Dara Albright Media covers everything from financial injustice; market bubbles; the rise, fall and resurrection of the small cap IPO; P2P investing; crowdfunding; investing red flags and how FinTech is changing the world – all in a style that is as appreciated by investing novices as it is by financial experts.

Access Articles

Connections

Dara Albright Events provide an unparalleled opportunity to accumulate gainful relationships as well as inestimable industry knowledge. Join us at future events.

Get Connected

Innovation

When Dara isn’t publishing thought provoking industry commentary or breaking new ground in the conference space, she is devising innovative strategies to help investors, businesses and financial services providers capitalize on the FinTech revolution. Let us help you!

Work With DaraAbout Dara Albright Media

We are in the early stages of a worldwide financial revolution which was ignited by technological progression and an intensifying demand for fairer financial systems. This uprising has sparked the FinTech ingenuity and legislative reform that continues to galvanize the crowdfinance movement.

As it snowballs, it is awakening the sleeping masses and empowering even more FinTech innovation. It is rapidly changing how we invest, raise funds, borrow, lend, pay for goods and services and save for retirement. It is reinventing currency, democratizing the flow of capital and giving rise to an entirely new generation of tech-centric financial leaders. This reconstitution of our financial system is creating opportunities for investors of all sizes, businesses in all stages of development and financial services providers of all echelons.

Dara Albright Media is dedicated to ensuring that all members of the financial ecosystem capitalize on this incredible transformation through fresh ideas, bleeding edge strategies, gainful relationships and a dose of inspiration.

Inspiration

Sometimes all it takes a touch of inspiration to formulate a new idea, complete an undertaking or even get you through a challenging day. Inspiration is everywhere! It can lurk within a verse of a song, a sentence of an article or even within an impromptu conversation.When I need a fresh dose, I can usually attain it from a stoic: one who transforms fear into prudence, pain into transformation, mistakes into initiation, and desire into undertaking. Here’s an inspirational read about a stoic – it also happens to hold the story behind my twitter handle: @tothestoics

Read "To The Stoics"

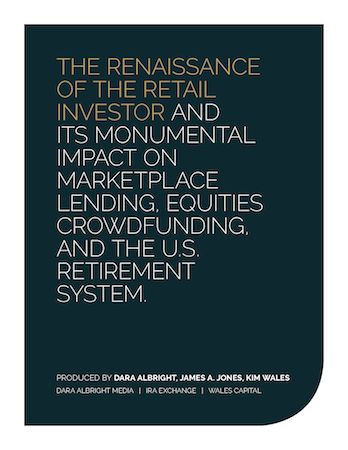

Groundbreaking New White Paper Illustrating the Magnitude of Tax-deferred Micro Alternative Investing

This white paper addresses the legislative changes being promulgated during the most prolific era for FinTech, and how, in confluence, these two dynamics have begun galvanizing retail investors – leading to seismic shifts in capital markets’ demographics and America’s retirement system.

Download

What People Are Saying…

From the Blog

Sharing the Inspirational Wealth

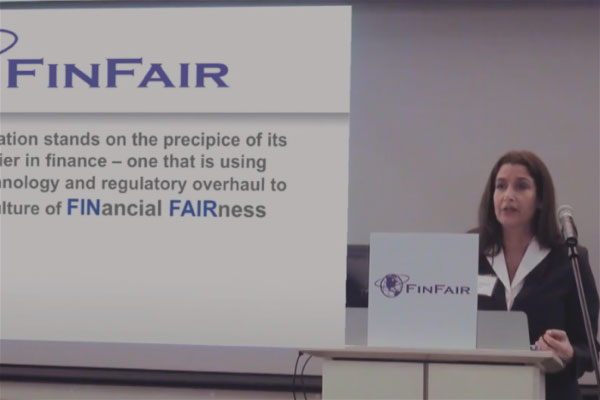

Last week I had the privilege of speaking at the Digital Asset Strategies Summit (DASS), in Dallas, where prominent institutional investors and industry thought leaders gathered to explore crypto investing strategies. To say that it was the most inspirational conference I had ever attended would be an understatement. I spent the entire day … Read More